The £78-billion hole in the UK that nobody wants to talk about

Key Points

- British households have redirected £78bn a year away from discretionary spending since the pandemic, roughly £2,700 per household

- Real-terms spending on restaurants, hotels and clothing has collapsed 30% since 2019/20 as essentials eat household budgets

- Top 40% of earners account for £20bn of the £24bn rise in annual household savings, choosing to save rather than spend

- EY now expects UK household consumption to grow just 0.3% in 2026 as renewed inflation hits spending power again

- Consumer-facing services have flatlined since 2024 while non-consumer services have pulled away, widening the gap

British households have quietly slashed £78 billion a year from discretionary spending since the pandemic, and the high street still hasn’t worked out how to win it back.

That’s the number buried in EY’s Spring 2026 UK Economic Outlook, and it explains why retailers, pubs, hospitality groups and consumer brands keep posting numbers that don’t match the “recovery” narrative politicians keep pushing.

The maths is brutal

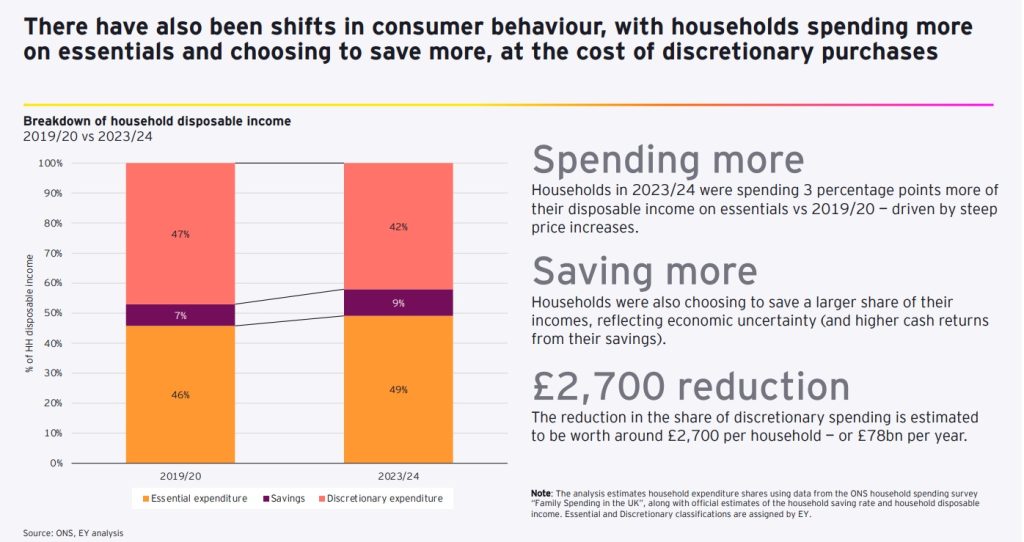

In 2019/20, the average British household spent 47% of its disposable income on discretionary purchases. Clothes, holidays, restaurants, the small luxuries that make life feel like more than survival.

By 2023/24, that figure had collapsed to 42%.

Essentials grew from 46% to 49% of household budgets as energy bills, mortgage payments and rent ate everything in their path. Savings rose from 7% to 9% as households braced for whatever came next. And discretionary spending? It got squeezed out.

That five-percentage-point shift translates to roughly £2,700 per household per year, or £78 billion across the country, redirected away from the businesses that depend on people choosing to spend rather than having to.

Where the money used to go

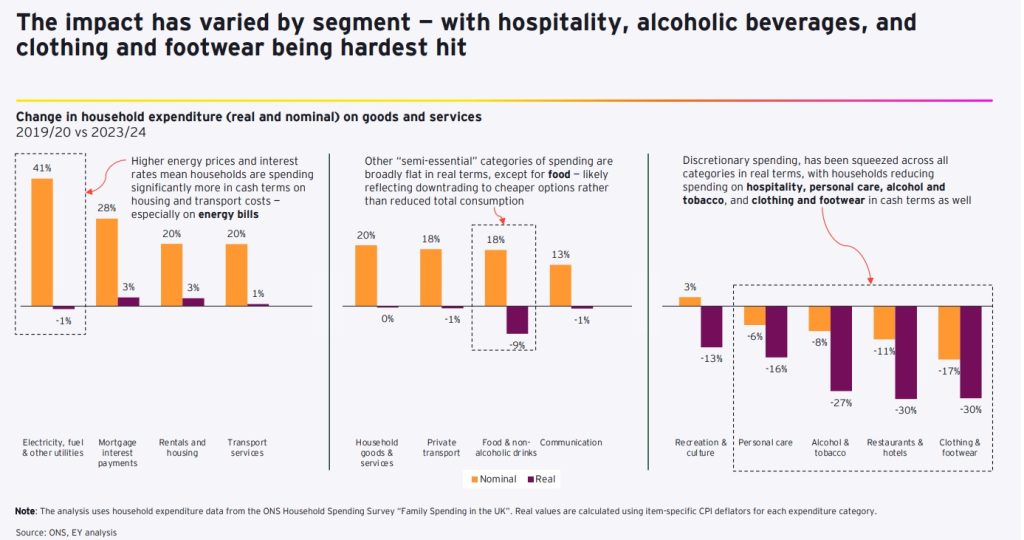

The carnage isn’t evenly distributed. EY’s breakdown of real-terms spending changes from 2019/20 to 2023/24 reads like a graveyard for entire sectors:

- Clothing and footwear: down 30% in real terms

- Restaurants and hotels: down 30%

- Alcohol and tobacco: down 27%

- Personal care: down 16%

- Recreation and culture: down 13%

Meanwhile electricity and fuel spending jumped 41% in nominal terms. Mortgage interest payments rose 28%. Rent climbed 20%. The British consumer hasn’t stopped spending. They’ve just stopped spending on things you’d want to invest in.

This is why your local pub closed. Why the Topshop site is now a vape shop. Why every restaurant group with a leveraged balance sheet has spent two years restructuring. The customers didn’t disappear. Their wallets just got rerouted to energy suppliers and the Bank of England.

The hospitality body count

Of every category in the basket, restaurants and hotels took the hardest hit in cash terms. A 30% real-terms drop in spending on a sector built on tight margins, expensive leases and even more expensive labour is, mechanically, an extinction event for a chunk of operators.

UKHospitality has spent the past 18 months warning about exactly this. The trade body reckons thousands of venues have closed since 2022, with the squeeze concentrated in independent operators who can’t absorb the way listed groups can.

The retail picture isn’t much prettier. Despite a modest recovery in 2025, the British Retail Consortium has been clear that consumer-facing services as a whole have flatlined since 2024 while non-consumer services (such as professional services, ICT, finance) have pulled away.

The savings glut at the top

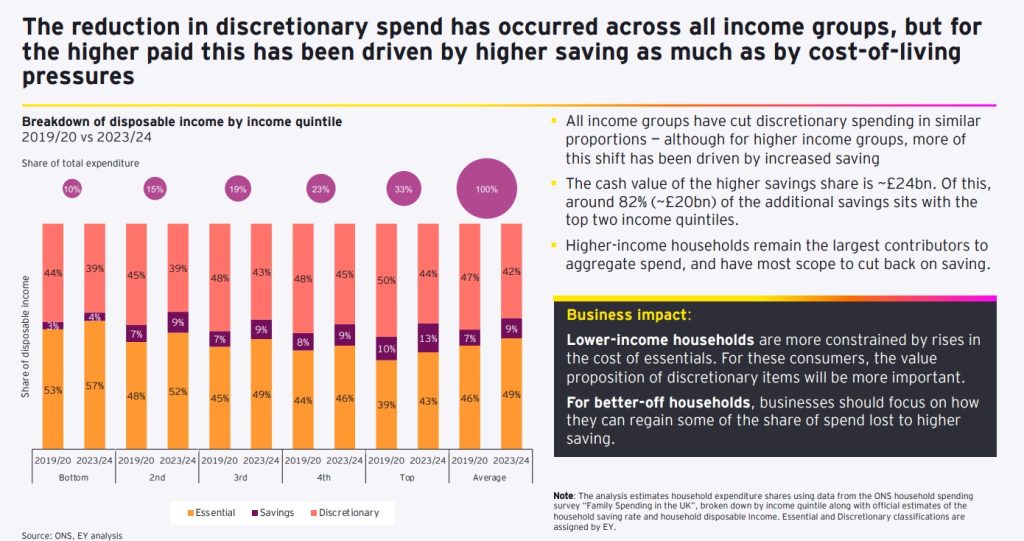

The reduction in discretionary spending hit every income group in similar proportions. But for the top two income quintiles, the shift wasn’t really about cost-of-living pressure. It was about saving.

Of the roughly £24 billion in extra annual savings British households now hold onto, around £20bn sits with the top 40% of earners. That’s not money that vanished.

That’s money sitting in NS&I accounts and high-interest savings products, waiting for someone to give people a reason to spend it.

So far, very few brands have managed to.

Why the recovery isn’t coming

The grim part of the EY analysis is that things are about to get worse.

The renewed conflict in the Middle East has driven oil and gas prices back up, with inflation now expected to climb above 4% by the end of 2026.

EY has cut its UK growth forecast to 0.8% for this year and 1.2% for 2027. Household consumption is forecast to grow just 0.3% in 2026 in real terms, down from 1.5% in EY’s pre-conflict baseline.

In plain English: the £78 billion hole isn’t getting filled. It’s getting deeper.

The strategic question for any consumer-facing business in Britain right now isn’t “when does demand come back?” It’s “how do I take share in a market that’s structurally smaller than it was?”

EY warns that for lower-income households, businesses need to nail the value proposition. These consumers will spend on discretionary items, but only when the maths obviously works.

For higher-income households, the challenge is psychological. They have the cash. They’ve chosen not to spend it.

Winning them back requires convincing them that whatever you’re selling is worth more than another month’s interest on the savings pile.

Most British retailers, restaurants and consumer brands are still pitching their offer to a 2019 customer who no longer exists.