Inflation has quietly wiped out 40% in British cash since 2004 – even with interest

Millions of Britons keep their savings in cash, viewing it as the safest option. But a new analysis from Barclays reveals a stark reality that over the past two decades, inflation has quietly eroded the real value of cash holdings by more than 40%, even after accounting for interest earned.

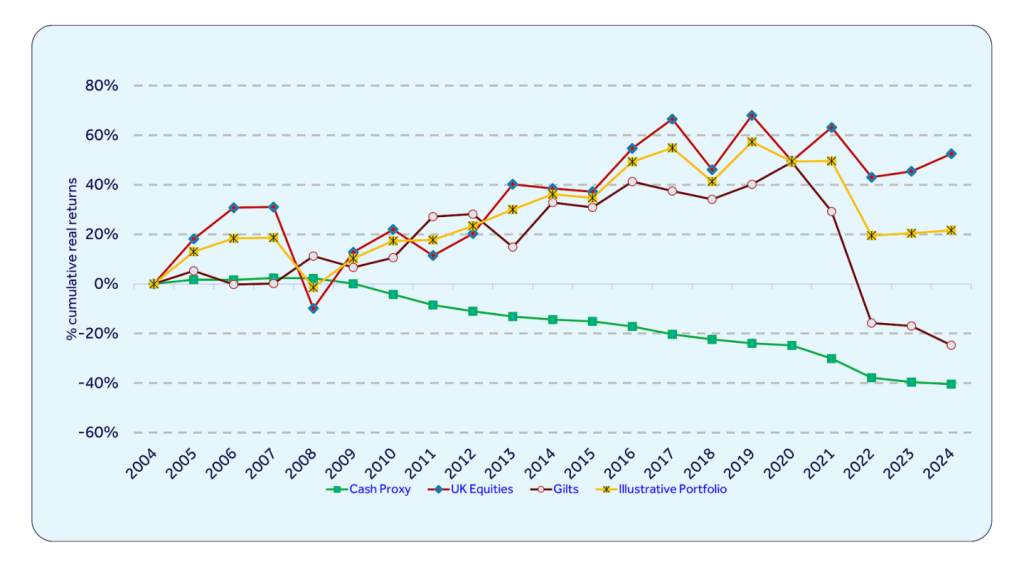

According to Barclays’ new paper, “The Missed Opportunity of Not Investing,” a proxy for holding cash in a typical building society account lost 40.5% of its purchasing power between 2004 and 2024.

That means £1,000 saved in cash in 2004 would have the spending power of just under £600 by the end of 2024.

The erosion happened gradually through the steady grind of rising prices outpacing the low interest rates paid on cash savings. Barclays used a proxy based on Nationwide Invest Direct Account-style rates, adjusted for inflation via its Cost of Living Index (gross of tax).

The hidden cost of caution

UK households hold substantial cash savings – potentially £610 billion that could be available for investment, up from around £430 billion late last year. For many, especially risk-averse savers, cash feels secure. Yet Barclays’s data shows the real risk to cash isn’t volatility but inflation.

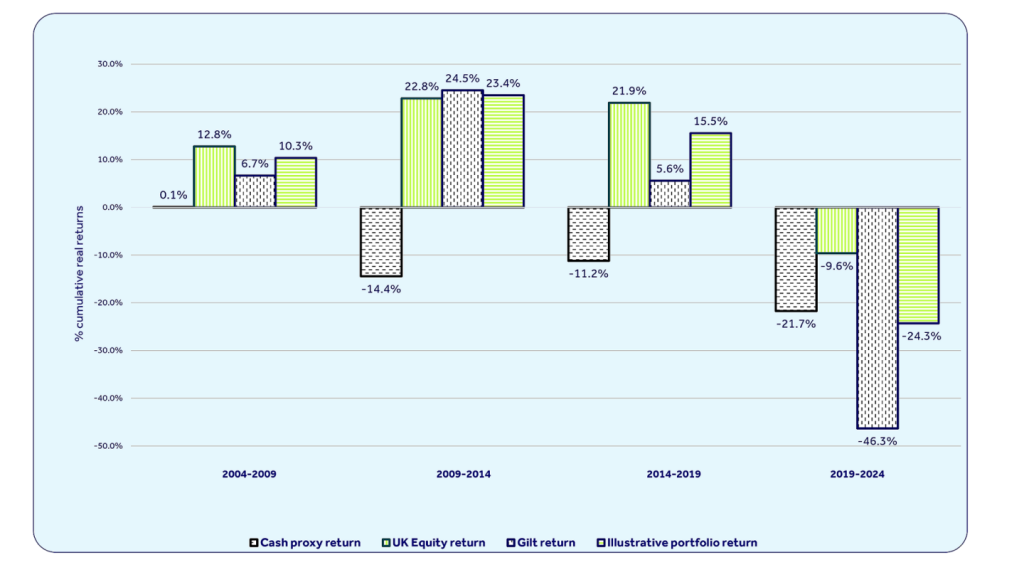

Over the same 20-year period, a simple illustrative diversified portfolio – 60% UK equities and 40% gilts (government bonds) – delivered a +21.6% real return after inflation and estimated fees of 0.80% per year.

UK equities alone rose 52.5% in real terms, while gilts fell -24.7%, highlighting the value of diversification despite periods of bond weakness.

The gap between the two approaches amounts to a 62.1 percentage point missed opportunity.

On average, cash holders gave up about 3.6 percentage points of annual real returns compared to the diversified portfolio.

Barclays drew on its long-running Equity Gilt Study, which tracks UK investment returns over 70 years. The 2004–2024 window captures major events: the global financial crisis, the COVID-19 pandemic, geopolitical shocks, and multiple inflation spikes, including the sharp rise in 2022–2023.

Cash showed persistent negative real returns across five-year increments, while equities delivered gains in most periods (with volatility), and the balanced portfolio provided moderate growth overall.