As tensions in the Middle East escalate amid the conflict involving the US, Israel, and Iran, disruptions to key shipping routes such as the Strait of Hormuz have driven significant volatility in Brent crude oil prices.

A new analysis from Oxford Economics warns that a sustained average of $140 per barrel for two months could precipitate mild recessions in several advanced economies, including the UK, while the US might narrowly avoid one.

The report, authored by Chief Global Economist Ryan Sweet and Director of Global Macro Research Ben May, uses simulations from the firm’s Global Economic Model (GEM) to explore potential outcomes.

It highlights structural differences in energy markets and policy frameworks that could result in the UK experiencing more pronounced effects from an oil shock, albeit with a temporal lag compared to the US.

The worst case scenario

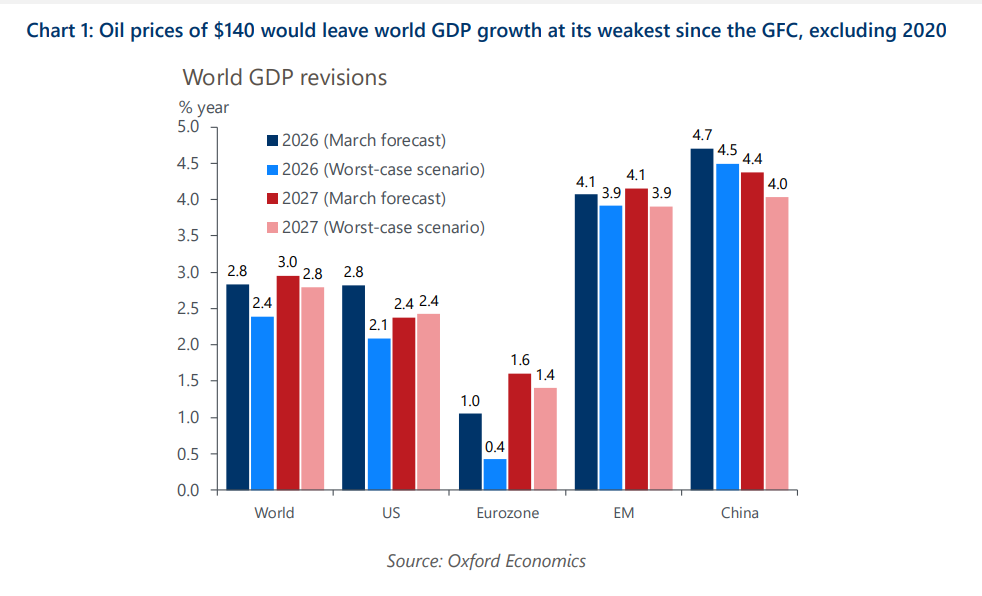

In Oxford’s low-probability “worst-case” simulation, Brent crude averages $140 per barrel amid prolonged closures or disruptions in the Strait of Hormuz, coupled with elevated natural gas prices.

This scenario incorporates spillover effects, including tightened financial conditions, supply-chain strains, and heightened inflation expectations.

The model projects a 0.7% decline in global real GDP by the end of 2026 relative to baseline forecasts, marking the weakest growth since the 2008-2009 Global Financial Crisis, excluding the 2020 pandemic.

The Eurozone, UK, and Japan are expected to enter mild recessions, characterised by output contractions and rising unemployment.

Emerging markets, however, demonstrate greater resilience, benefiting from energy subsidies, price controls, and gains for non-Middle Eastern oil producers.

Global consumer price index (CPI) inflation is forecasted to peak at 5.8%, below the 8.9% high following Russia’s 2022 invasion of Ukraine, due to comparatively milder annual energy price spikes and less severe supply disruptions.

“The economic cost of higher oil rises as the price increases due to the growing likelihood that the spike triggers factors such as second-round inflation effects, broader tightening in financial market conditions, and supply-chain disruptions,” the report states.

The UK’s delayed vulnerability

The UK’s exposure stems from its reliance on imported energy and the mechanics of its domestic pricing system.

Energy bills are adjusted quarterly under regulatory caps, meaning the inflationary impact of peak oil and gas prices in April and May would not fully materialise until the 1 July reset.

Consequently, UK CPI inflation is projected to surge later in the year, exacerbating pressures on real disposable incomes and consumer spending through the second half of 2026.

This delay postpones recessionary forces but intensifies them when they arrive.

The report anticipates a mild UK contraction, compounded by supply-chain disruptions affecting imports of energy, aluminium, and petrochemicals from Gulf Cooperation Council countries.

Global equity markets could decline by approximately 10% in the second quarter, though the wealth effect on UK households is less pronounced than in the US due to differing asset ownership patterns.

In response, the Bank of England is expected to raise interest rates by 25 basis points this year, reflecting a hawkish shift to counter inflation averaging 2.5 percentage points above baseline in the latter quarters. This tightening could further constrain business investment and economic activity.

By comparison, the US economy is projected to approach but not enter a recession, with growth stalling temporarily and unemployment rising moderately.

Key indicators monitored by the National Bureau of Economic Research (NBER), such as industrial production, personal income, consumer spending, and employment, would signal an economy on the brink.

A more moderate risk

The economists also looked at a higher-probability alternative where oil averages $100 per barrel for two months, incorporating milder secondary effects such as delayed rate cuts rather than hikes.

Global GDP would be 0.2 percentage points lower than baseline by the fourth quarter, with inflation moderately elevated but no recessions triggered.

This scenario aligns with recent price trends and ongoing Strait disruptions, underscoring upside risks to the baseline forecast of $80 per barrel in the second quarter.

Leave a Reply