A UK family of four could amass a tax-free investment portfolio worth over £1 million in just a decade by maximising contributions to ISAs and Junior ISAs, according to a new analysis by investment platform AJ Bell.

The strategy relies on the power of consistent saving, tax-free compounding, and long-term investment in low-cost global funds – turning regular contributions into substantial wealth through growth over time.

The family setup and tax-free vehicles

Consider a typical family: two adults and two children. In the current tax year (2025/26), each adult can contribute up to £20,000 annually to a Stocks and Shares ISA, while each child qualifies for a Junior ISA allowance of £9,000 per year.

That totals £58,000 in combined annual contributions (£20,000 × 2 adults + £9,000 × 2 children)—all sheltered from income tax, capital gains tax, and dividend tax.

Anyone (parents, grandparents, relatives, or friends) can contribute to a child’s Junior ISA, up to the £9,000 limit, with the funds locked until the child turns 18. At that point, the account converts to an adult ISA, giving the young person control over a potentially significant nest egg.

The investment approach

AJ Bell’s analysis assumes the money is invested in a low-cost global tracker fund, such as the Fidelity Index World fund, which provides broad exposure to worldwide equities.

Key assumptions include:

- Annual net growth of 5% after charges (a conservative estimate for long-term equity returns).

- Or 7% for more optimistic scenarios (closer to historical averages for global stocks, though not guaranteed).

Contributions are made consistently each year, with no withdrawals, allowing compounding to work its magic.

Real-world example: Hitting £1 million in about 10 years

AJ Bell examined historical data starting from the 2016/17 tax year, when allowances were lower (£15,240 per adult ISA and £4,080 per Junior ISA).

Even with those smaller starting limits, and gradual increases to today’s levels, a family maximising allowances every year could have built a portfolio worth £1,083,174 by the end of February 2026.

This real performance demonstrates the strategy’s potential, as the invested funds benefited from a decade of market growth.

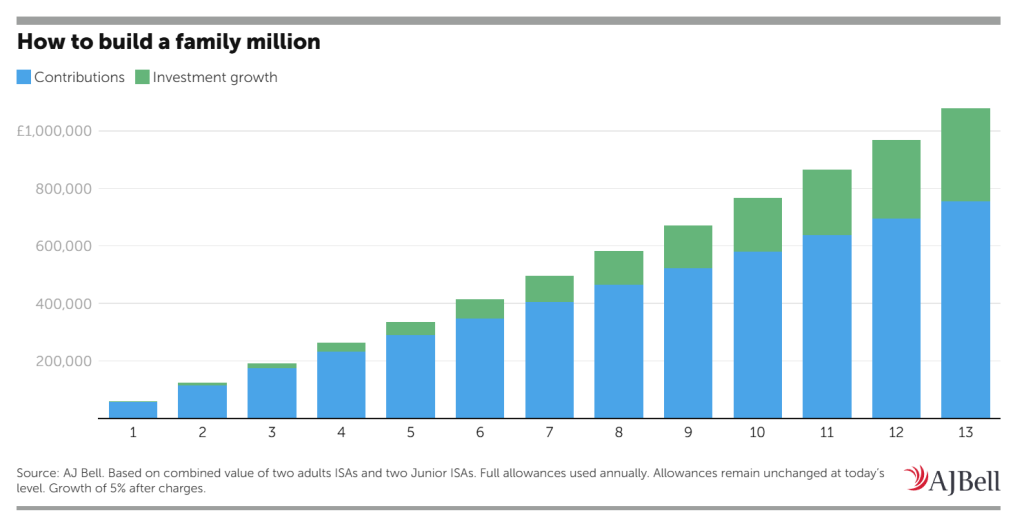

For a forward-looking projection starting now with the full £58,000 annual allowance:

- At 5% annual growth, the family portfolio would exceed £1 million in around 13 years (reaching approximately £1,079,000, with roughly £744,000 in the adults’ ISAs and £167,500 per child’s Junior ISA).

- At a stronger 7% growth rate, the £1 million milestone arrives in just over 11 years.

More accessible scenarios

Not every family can commit £58,000 annually, this requires significant disposable income. AJ Bell also modelled more realistic lower contributions:

- £34,000 per year (£12,000 per adult + £5,000 per child) at 5% growth reaches about £1,004,000 in 18 years.

- Even £27,500 annually at 7% growth gets to £1 million in 18 years.

The message is clear: starting earlier, contributing as much as possible, and staying invested long-term dramatically shortens the path to seven figures.

Why this works – and the caveats

The secret sauce is tax-free compounding. Without tax drag on gains or dividends, more money stays invested and grows exponentially over time.

However, AJ Bell stresses important risks and realities:

- Market returns are not guaranteed – past performance (including the strong decade since 2016) doesn’t predict the future, and values can fall as well as rise.

- ISA allowance rules could change in coming years.

- Few families can afford the maximum £58,000 yearly; the strategy scales down but extends the timeline.

- This is a long-term approach requiring discipline and no early withdrawals.

AJ Bell’s analysis highlights how accessible tax wrappers like ISAs and Junior ISAs, combined with disciplined investing, can help ordinary families build serious wealth, potentially turning a family of four into millionaires through smart, consistent use of these simple accounts.

Investing involves risk. The value of investments can go down as well as up, and you may get back less than you invest. Tax rules can change and depend on individual circumstances. This is not personal advice.

Leave a Reply