Here’s what Labour’s new property tax could look like

Over the past week, and in advance of the autumn Budget, the government has been testing the reaction to potential property tax changes.

While no formal announcements have been made, the proposals under consideration suggest a willingness to overhaul a system which is, for the most part, remained unchanged for decades.

The reforms aim to raise revenue, improve fairness, but most of all, boost economic growth – but each comes with trade-offs.

In an analysis of the proposed changes, property group Hamptons considered the planned introduction of Capital Gains Tax (CGT) on residential property sales above a certain threshold

While the exact level is yet to be confirmed, The Times suggests the government is considering applying CGT to primary residences sold for more than £1.5 million. Currently, only second home sales command a CGT rate of 24% for higher-rate taxpayers and 18% for basic rate.

“This change would mark a fundamental shift in how property is taxed—potentially moving away from taxing purchases to taxing profits,” Hamptons said.

“The logic is clear, taxing gains is arguably more progressive, targeting wealth accumulation rather than mobility. But the implications could be far-reaching.”

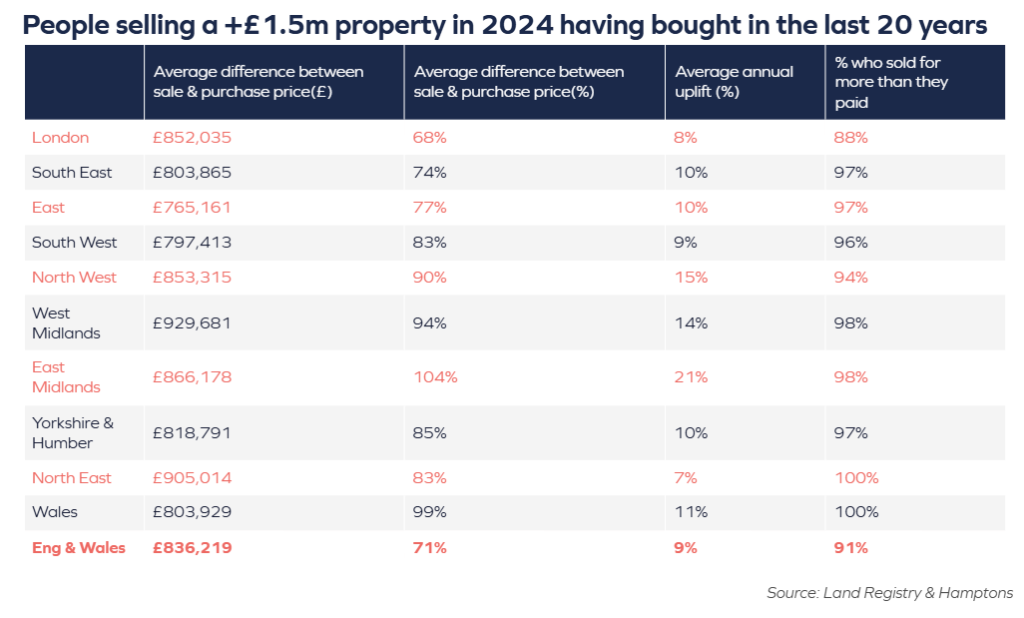

The group’s analysis shows that just 1.0% of homes sold in England over the past 12 months exceeded the £1.5 million mark, which would limit the number of households impacted by the change. Yet those sellers achieved, on average, a gross gain of £836,200 compared to what they originally paid.

“That’s a substantial uplift—and whilst there will likely be costs that can be offset, it could translate into a hefty tax bill if CGT were applied. In fact, 91% of sellers in this price bracket sold for more than they bought, underscoring the scale of potential liability.

“The regional skew is stark. In 2024, 81% of all £1.5m+ sales were concentrated in London and the South East. In contrast, across the other regions, £1.5m+ sales make up less than 0.5% of all sales.”

This means the proposal would disproportionately affect homeowners in the South, many of whom may have owned their properties for decades and seen values rise through long-term inflation and market growth, Hamptons said.

While the headline gains may appear substantial, they often mask a slower pace of appreciation. For example, the average annual uplift for £1.5 million+ sellers in London was 8% over the past 20 years. In some cases, house prices haven’t kept pace with inflation.

“This is particularly true for those who have bought homes in central zones during the past decade. For these households – especially those who don’t need to move – the prospect of a CGT bill could act as a tax on inflation and a disincentive to sell,” Hamptons said.

There’s also the risk of behavioural distortion. A hard threshold at £1.5 million could create a cliff edge, with sellers pricing just below the limit to avoid tax, and buyers steering clear of homes that might tip them over.

This could reduce liquidity in the upper end of the market, dampen transactions, and ultimately weigh on house price growth and Treasury revenues alike, the group warned.

“In theory, taxing gains rather than purchases could improve mobility—especially below the threshold. But in practice, unless inflation-adjusted, it risks penalising long-term ownership and may introduce new frictions into an already complex market.”